Source: NAHBNow, the news blog of the National Association of Home Builders. Reprinted with permission. https://bit.ly/21Lumber

While the price of framing lumber has dropped roughly 50% over the past seven weeks according to Random Lengths, prices paid by builders have declined by a fraction of that amount. The disconnect — which has always existed — is inherent to the lumber supply chain.

This post outlines the reasons why when lumber market prices drop sharply there can be a long lag time before these full price reductions trickle down to builders and why higher prices reach builders with a much smaller lag time when the price of lumber increases.

The Lumber Supply Chain

The supply chain for dimensional lumber typically consists of five stages.

1. Timber is harvested from the forest and shipped to a sawmill.

2. Saw logs are cut to dimension at the mill and shipped to a distributor.

3. The wholesaler delivers to lumber retailers such as lumberyards and building materials suppliers.

4. Customers purchase the product to use as a production input.

5. The end-user (e.g., home builder) constructs a home.

A lumber company may operate at one stage or multiple stages. In the latter case, the firm is said to be vertically integrated— such structure is commonplace in the lumber industry. For example, large lumber companies may own:

• timberlands from which they get logs,

• mills at which they cut (and may also plane) lumber, and

• a distribution network or building materials supply company.

Sources of Price Timing Differences

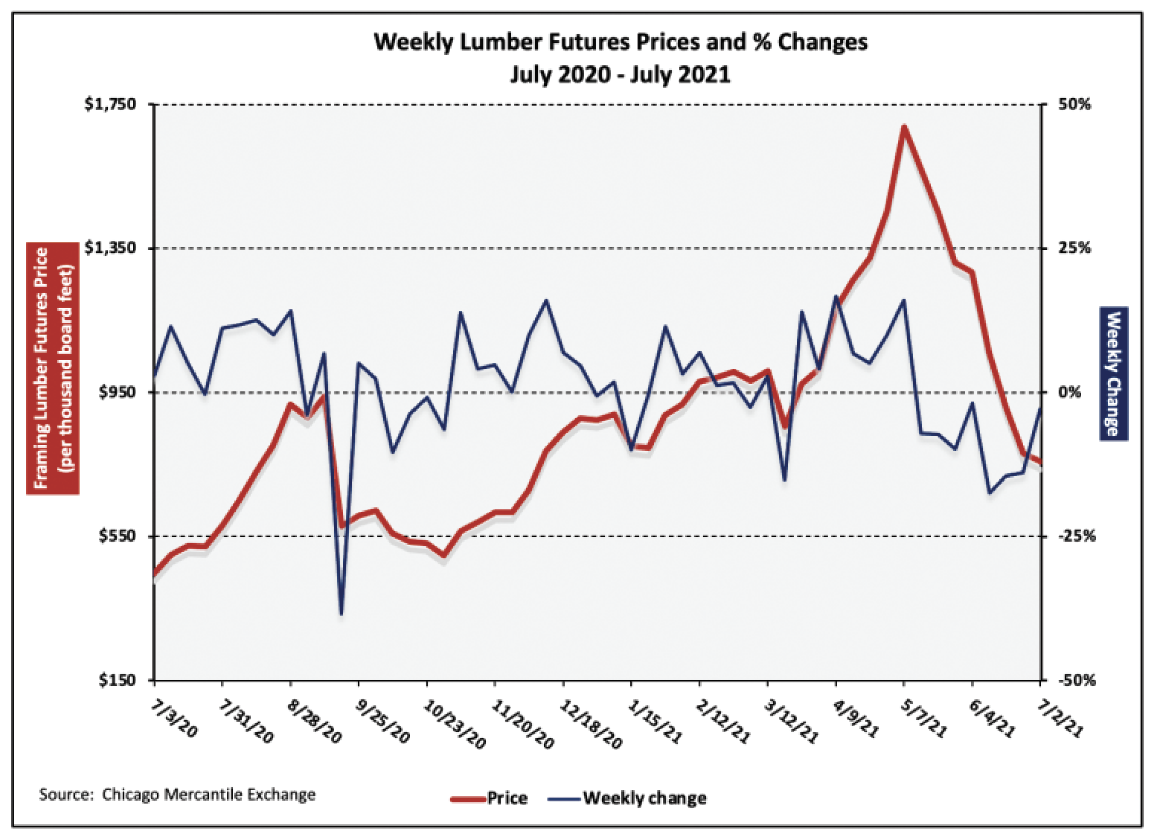

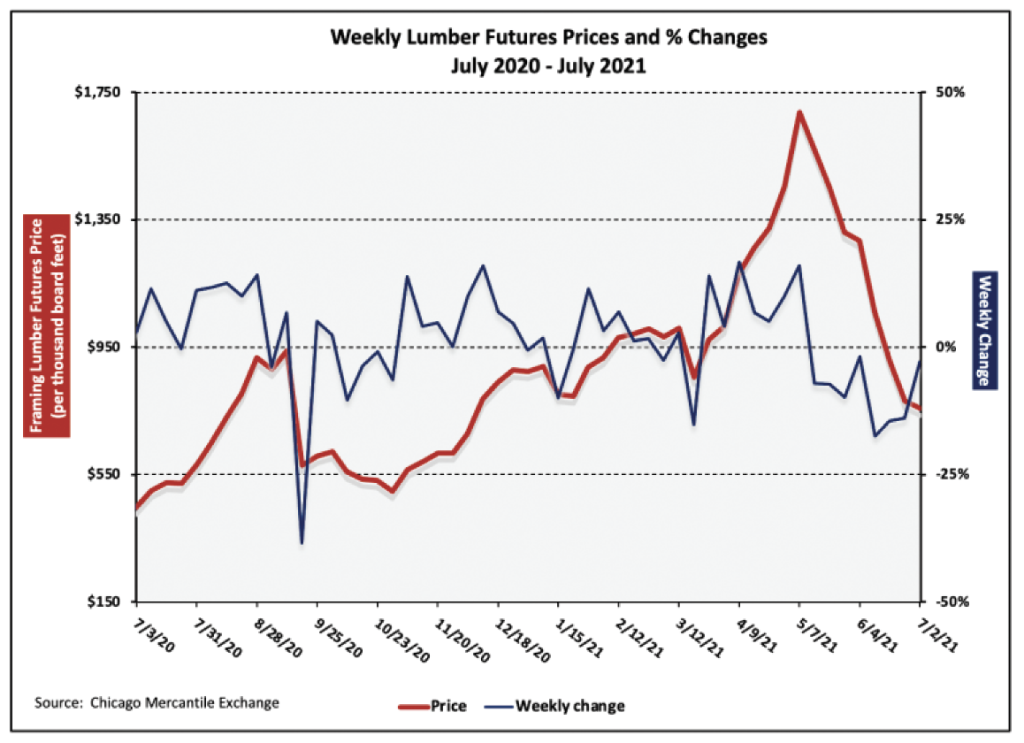

Coverage of the recent fall in lumber prices — usually proxied by futures in the media — began in May. Indeed, the price of July lumber futures has declined 56% since peaking on May 10 and by 46% since May 14 (the final trading day of May 2021 futures contracts).

As the price declines began grabbing headlines, however, the price of lumber packages quoted to builders held at record highs. In economics jargon, prices paid by builders — or “street” prices — were “sticky.” This dynamic is primarily due to dealers’ inventory carrying costs and potentially large differences between the price at which inventory is bought and sold.

To maintain margins, retailers and wholesalers do their best to buy low and sell high. At the very least, they try to avoid buying high and selling low, which happens to be the biggest risk in an environment of rapidly falling prices. For example, had a lumberyard quoted a client at prevailing prices two weeks ago, it would be taking a 25% loss relative to current pricing. Thus, a supplier that quotes clients at current market prices will consistently lose money when prices are falling.

Suppliers’ inventories will also tend to be tighter during periods of falling prices. Whatever inventory the business has on hand was expensive relative to current prices. This gives wholesalers and retailers incentive to run through that inventory while they can still get close to what they paid for it — and doing so without souring relationships with customers. And for reasons stated above, they will be “trigger shy” to buy more lumber than they are contractually obligated to provide to customers for fear of ending up with a load of inventory on which they will take a loss.

When Do Lower Prices Reach Builders?

Home builders and remodelers begin to get price relief once mill prices have substantially decreased for an extended period and/or stabilized. Note that large price decreases alone may not be sufficient. Prices must fall for long enough to materially lower a supplier’s average costs after a run-up. Depending on the rate and consistency of price decreases and whether prices have stabilized at the lower level, it may take a few weeks to a couple of months for builders to see price relief on the order initially reported in the futures or cash markets.

The length of this “waiting period” varies with builder size, supplier size, and the specific builder-supplier relationship. Buying power is positively correlated with the size of a residential construction firm while the same is true for suppliers’ seller power, all else equal. The relative difference in market power between the buyer and seller is crucial in determining how quickly lower prices transmit to a customer.

Personal and business relationships also influence timing. Home building is an industry that is highly dependent upon relationships both with customers as well as vendors (which is why most building materials dealers belong to their local builders association). The length and quality of a builder-vendor relationship can positively affect how soon the builder is quoted lower lumber prices.

Why Do Builders’ Lumber Costs Increase with Market Prices?

In contrast to the dynamics of an environment with falling prices, higher prices reach builders with a much smaller lag when market prices are increasing. The same forces that lead to large lags relative to mill prices on the way down can help explain why builders’ lumber costs may increase in tandem with mill prices.

Wholesalers tend to be “trigger happy” when prices skyrocket. As the cost of their inventory is low relative to cash prices during these periods, they will quote at or near current market prices. The environment is one in which wholesalers are assured to buy low and sell high.

However, wholesalers cannot predict when a bull market is going to end and buy their lumber according to how likely they believe it will last. As different buyers may have different forecasts, disparities in purchasing behavior can arise. A wholesaler that assumes lumber prices will keep rising for two months will buy more inventory than one assuming the run will last for two weeks.

Retailers generally have less buying power than wholesalers have selling power. In such a scenario, the retailer (e.g., lumberyard) is said to be a “price taker.” As a result, their inventory costs tend to increase in step with market prices. These higher costs are passed on to builders in order to maintain positive operating margins. Thus, lumber retailers are less likely than wholesalers to realize outsized profits when prices are rising.

NAHB economist David Logan provides further analysis on the lumber supply chain in this Eye on Housing blog post: https://eyeonhousing.org/2021/07/why-builder-lumber-prices-remain-higher-than-headlines-suggest/. FBN